Dear client,

Given the exceptional circumstances caused by the outbreak of war in Ukraine, I have decided to draft my quarterly letter early in order to explain the measures we are taking to protect the value of the assets you have entrusted to us.

To begin, we share your concern about a situation that, until recently, seemed unimaginable, one reminiscent of the darker days of our past. In our mission to protect your wealth, the question arises: what to do? Unfortunately, the scenarios that lie before us in the immediate future are not very encouraging, since we can only realistically envision one “bad” scenario and another “very bad” scenario.

The “very bad” scenario would entail an expansion of the conflict due to an uncontrollable incident. It is unlikely but, given the current circumstances, not impossible: think of the attack on the nuclear power plant last week. The thought prompts fear and anguish, and the consequences for any asset class would be widespread and devastating: all investments would lose value. As difficult as it is to state thusly, we have decided to discard it from our decision-making process in order to focus with cold determination on the “bad” scenario. And what does this entail?

Once fully recovered from COVID-19, the economy will likely see lower growth for the duration of the conflict, as well as an upswing in inflation due to the increase in energy, commodity, and food prices. The solution to reduce or eliminate that dependency will require time and money. Moreover, the central banks (especially the ECB) face a serious dilemma given that a tightening of monetary policy—expected until only recently—could further complicate matters.

Our response to this "bad" scenario is consistent with our investment style, meaning, it comes down to the companies in which we invest. Though this work is ongoing, we have proceeded to review the investment thesis of each company in light of the new situation, in a process of reorganisation and optimisation, eliminating those that seem to be more adversely affected by i) energy prices, ii) the cyclical nature of the business, and iii) relevant exposure to the Russian market. In reality, there are very few, given our well-known preference for quality companies.

Alternatively, we have taken advantage of falling prices to invest or strengthen investments in companies of extraordinary quality, whose previous overvaluation impeded their purchase. This opportunity emerged last week as the massive sell-off on stock markets, especially in Europe, triggered price declines. It is worth remembering that the companies in which we invest have global sales profiles and, consequently, their European domiciles obscure the vast geographical diversification of their businesses. We have also taken the opportunity to reduce certain US positions, dispensing with those whose business models appear vulnerable.

The equity positions of your portfolio trade at multiples (P/E ratios) similar to those of March 2020, when the global economy came to a standstill due to COVID-19. Though this does not guarantee the short-term performance of the investment, it does significantly reduce price risk going forward.

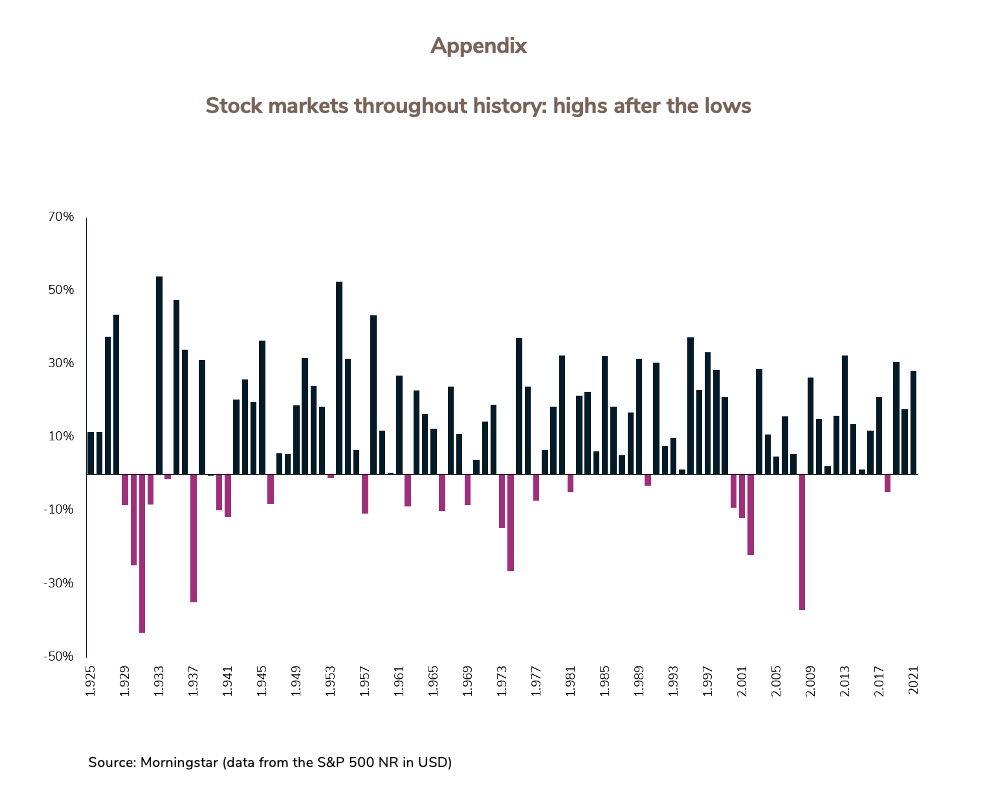

It is also worth remembering that the value of a company is not extinguished by an uptick in fear of the unknown, or a rise in the risk premium. These factors affect price, but value relates to the expected long-term benefits that, in our selection, remain intact. We therefore consider them to be true “repositories of value”, beyond any potential slowdown in 2022 profit growth, which is possible. It is highly likely that this value will emerge once the “very bad” scenario vanishes from investor sentiment (see Appendix).

To conclude, I would like to share a reflection that the war in Ukraine has come to symbolise a new world order dominated by greater geopolitical risk, a development we have warned of for many years. In this environment, I feel that our firm convictions based on the individualised analysis of investments will be rewarded, because going forward quality will be more necessary than ever and, though scarce, our portfolios have it in abundance.

Though they may not allay your concerns about the state of the world, I trust these words will instil some sense of confidence because, since it is not “the end of the world”, your portfolio has tremendous upside potential.

Many thanks for your trust,

Sincerely,