Dear client,

The war in Ukraine has crystallised some latent trends, swinging the pendulum of history toward scenarios more akin to those of the 1970s and 80s.

History returns

At EDM’s 25th anniversary celebration in 2014, we said, “The world we live in has brought back all the "isms" and the political risks are increasing. Whoever said we have entered the end of history [Francis Fukuyama] was wrong.”

Fukuyama himself says the war in Ukraine has made the “rebirth of freedom” possible. And former US Secretary of Defence, Robert Gates, stated, "The war has ended Americans’ 30-year holiday from history.”

The war will bring serious short-term ramifications: lower economic growth and higher inflation due to the rising cost of energy, metals, and food. But it is the long-term consequences that will be of greater significance. In my opinion, the most important will be:

1. A return to a world fragmented into blocks, or economic and trade barriers. Will it signify a setback in globalisation?

2. Prioritising the security of output and transport above cost.

3. Urgent increase in EU defence spending that will put a strain on public finances.

4. Massive efforts to achieve energy independence by diversifying supply sources.

5. Difficulty in reconciling energy security and climate transition (Paris 2050 goal).

The good news is that we have witnessed a sudden awakening from European naiveté (primarily German) in the belief that trade necessarily brings peace. The European Union has acted quickly both in terms of military spending and finding a path to mitigate energy dependence on Russia.

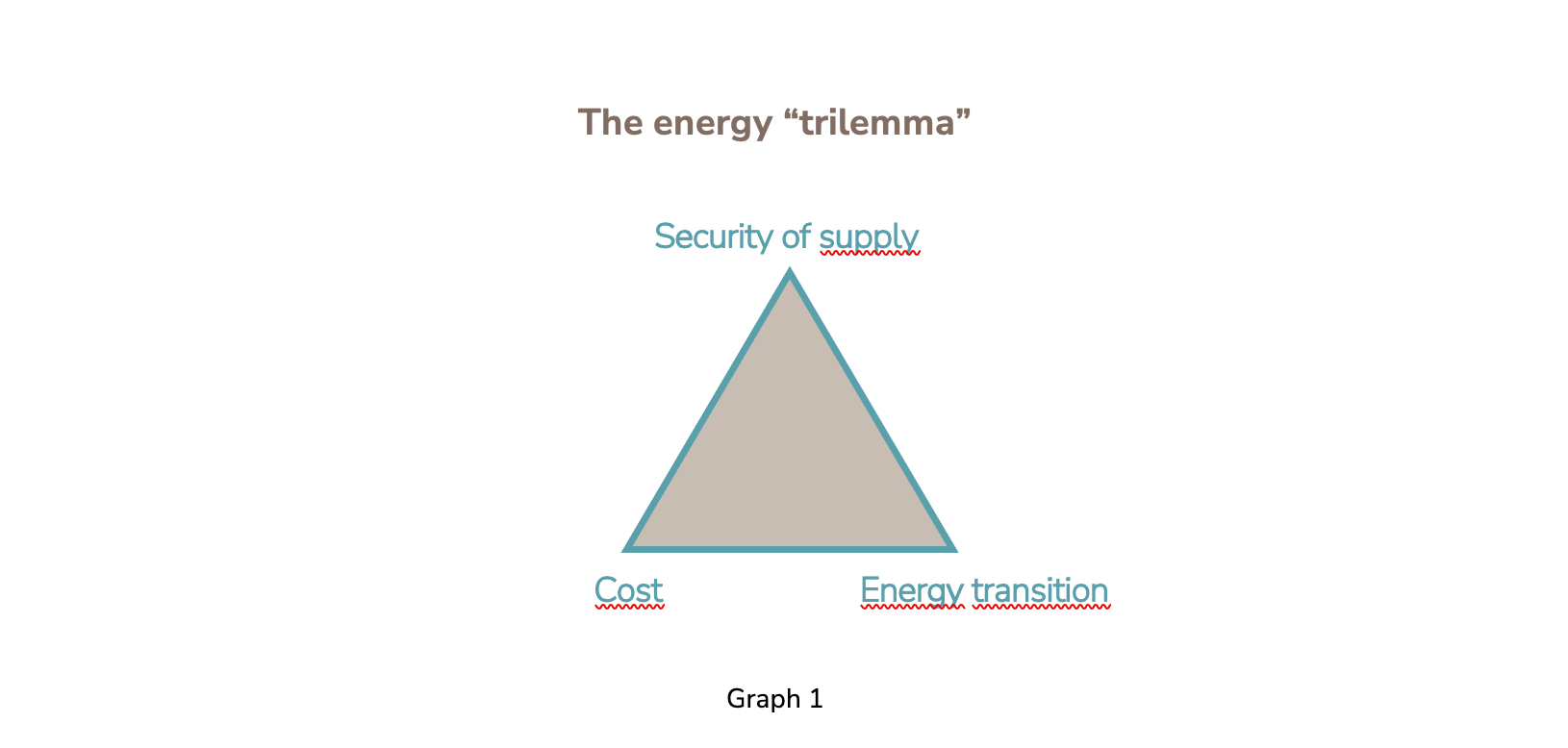

The latter brings us to a "trilema", a situation wherein, of three desireable objectives (Graph 1), only two can be achieved. In this case, the priorities will be security of supply and compliance with the decarbonisation goal (CO2), which will trigger an increase in the cost of enrergy.

The combination of these factors has an unequivocal inflationary air, whose most similar precedent is the post-WWII period in which supply failed to immediately cover neglected demand, much like our current post-COVID, war-in-Ukraine environment.

Demanding environment: Quality will be rewarded

All of this seems to foreshadow a less favourable geopolitical and economic environment in the years to come than that which we have enjoyed for the last three decades, characterised by (a) low interest rates; (b) low corporate taxes; (c) and the globalisation of production and trade. Recognising a change in panorama is necessary but it is not the end of the world and we do not believe it will trigger a recession. It will, however, require that investors be more discerning when selecting assets and exercise more discipline in their valuations.

EDM’s investment style, which emphasises stock picking rather than predicting short-term market trends, does not require us to make changes in light of this new scenario. On the contrary, our ongoing search for top quality assets—our distinguishing feature—will produce the desired effect: protecting our clients’ assets. Quality, which is scarce, has consistently been and will continue to be rewarded (Table 1).

Equities: growing profits, shrinking multiples

Though direct exposure to Russia and Ukraine is minimal among our selected companies, we have seen that the second and third round of effects can be significant and will dominate the investment scene in the years to come.

To begin with, it is important to acknowledge that, though medium-term inflation expectations currently seem overvalued, higher interest rates and increased geopolitical risks (risk premium) will weigh on equity valuations by reducing the present value of future profits. In fact, this phenomenon, known as multiple (P/E ratio) compression, already occurred in Q1 2022.

In some cases during the quarter (14.3.2022) we saw real declines creating great opportunities. To the extent that the portfolio had available liquidity, we have capitalised on them. And when liquidity was not available, we optimised portfolios by concentrating on companies with maximum visibility for their businesses in the years ahead.

Still, it is important to avoid oversimplifications. The past does not prove that, in a phase of tightening monetary policy, the results of investing in equities will necessarily be negative since the profits of many companies grow with inflation and thus offset declining multiples.

Bonds: flattening of the curve

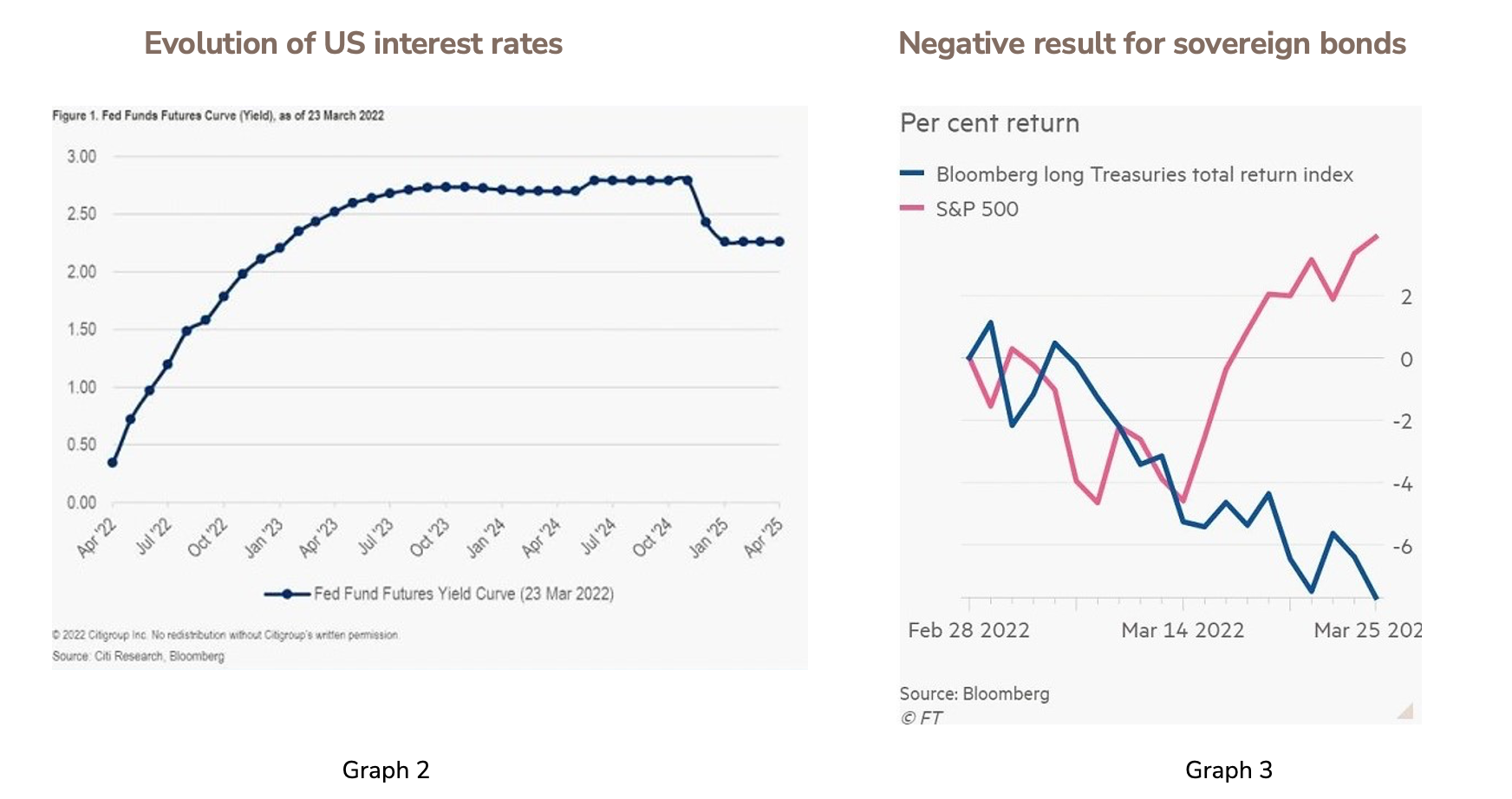

As regards bonds, in the last fortnight, statements from the Fed chairman seem to indicate greater resolution in raising interest rates (Graph 2). The reaction of investors has been to demand higher yields for all terms, from two to 10 years. This phenomenon, known as the “flattening of the curve” has heralded lower economic growth in the past.

Investors, fearful of future inflation, have demanded higher yields from bonds and, because yields increase as market prices fall, the total return on 10Y US Treasury in Q1 2022 was -5.79% (Graph 3), while the German Bund hit -6.36%. Volatility especially affects long-dated bonds.

Volatility is high for equities and bonds

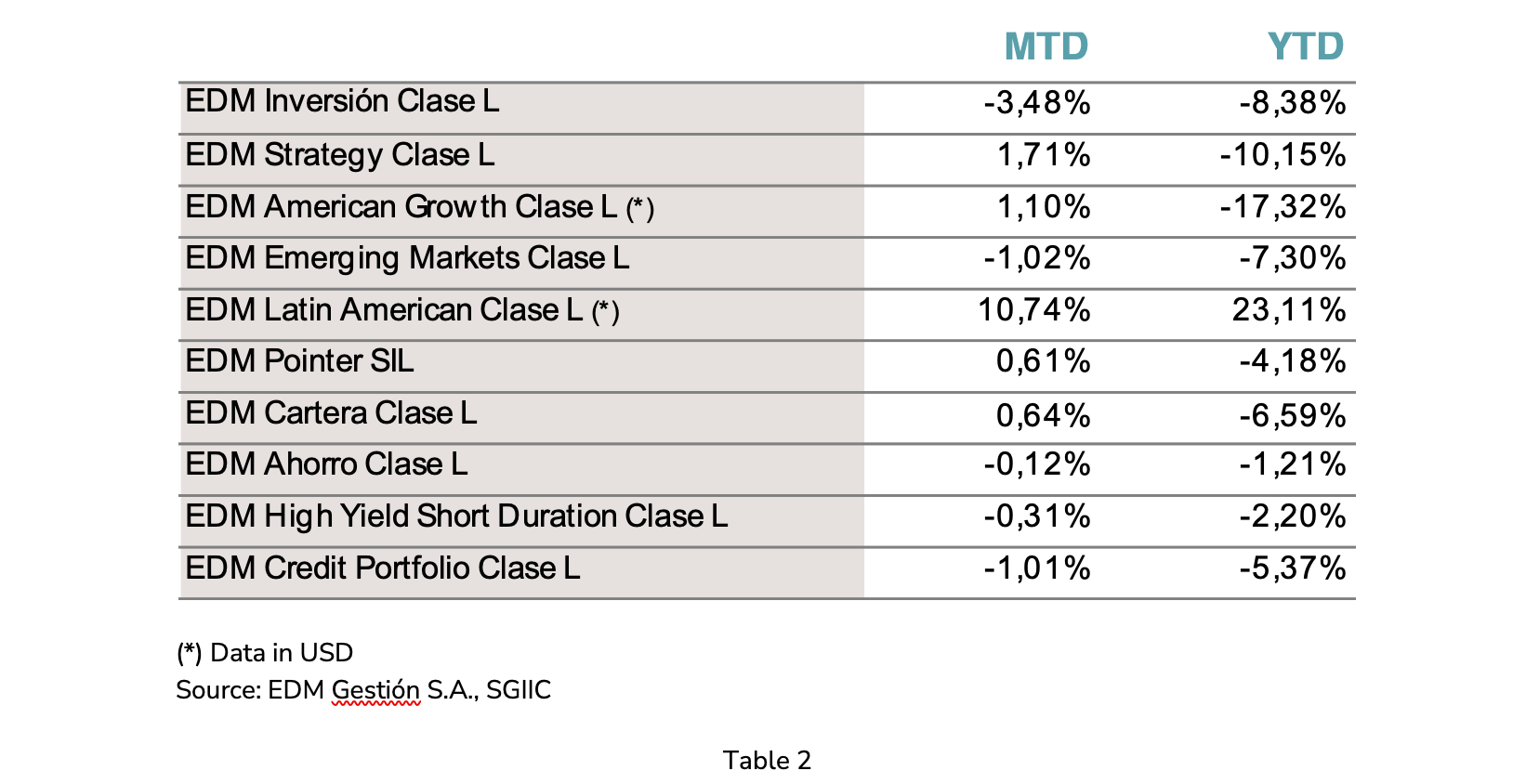

In March, stock markets regained the territory lost since the outbreak of the war on 24 February with strong market rebounds, though not enough to completely absorb the declines of the first two months of the year. Table 2 shows the performance of EDM’s funds as of 31.3.2022.

A reflection for investors: combatting uneasiness

The world is at a difficult crossroads amid geopolitical tensions and severe energy price and supply challenges. This framework of considerable uncertainty precipitates restlessness and discomfort that are a prelude to fear, prompting many investors to sell-off positions at the worst possible time (first fortnight in March) and wait for the situation to improve. By the time it does, the market will already have anticipated it.

Time and again history proves that anticipating the market is difficult and, in general, does not yield long-term results. In fact, it is a gift for those of us, like EDM, who put emotion aside and are guided by our convictions, based on the fundamentals of the investment.

Many thanks for your trust.

Yours sincerely,

Eusebio Díaz-Morera