Dear client,

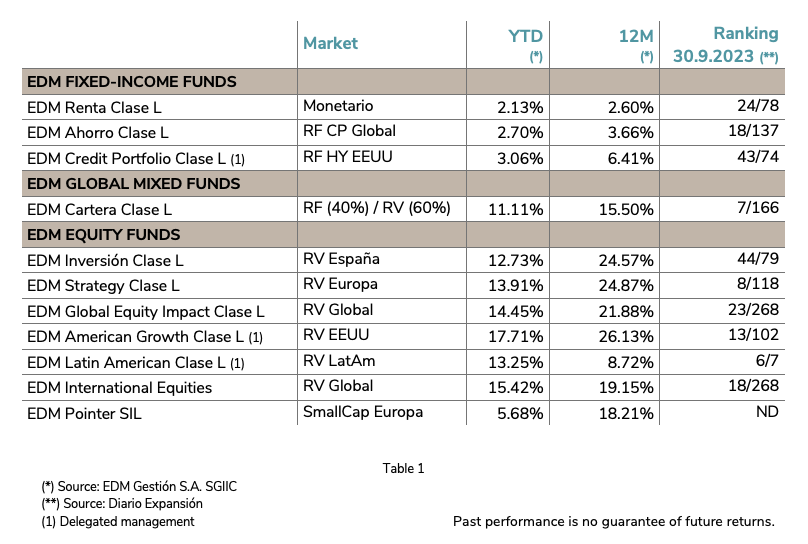

Twelve months after the stock market low of September 2022, indices have recovered the majority of valuation declines registered at the time. With the summer quarter—dubbed the “silly season” by some—behind us, the results of EDM’s funds corroborate our confidence in the assets selected and our unwavering scepticism of those who claim to “know” what the market will do (see Table 1).

Those who, on the advice of Charles Munger (partner of W. Buffett), weather moments of maximum pessimism with strength of character have benefitted from these favourable results. According to Munger, the long-term power of compound interest has only one enemy: the unnecessary interruption of its job (i.e.: selling unnecessarily).

Those who took the time to read the news and follow the statements released over the summer will agree that the central banks and their representatives have monopolised the movements of the stock market... and sovereign debt!

The results for our funds and portfolios at the September close, detailed in Table 1, are attributable to several factors:

A) Equities

- EPS growth relative to 2022, despite high percentage growth last year

- Anticipation of a shift in monetary policy, with a decrease in interest rates

- Sharp appreciation of tech companies

B) Bonds

- The drag of interest-rate hikes, especially in the shorter term

- Attractive yields for all maturities, with potential appreciation in the longer term if monetary policy shifts

In the letter from our Chair dated 30 June, María Díaz-Morera specified the criteria that, given prior evolution, dominate our investment policy, namely:

- Asset diversification

- Non-negotiable quality, in both equities and bonds

- Discipline with regard to valuation, to avoid overpricing

FRAME OF REFERENCE

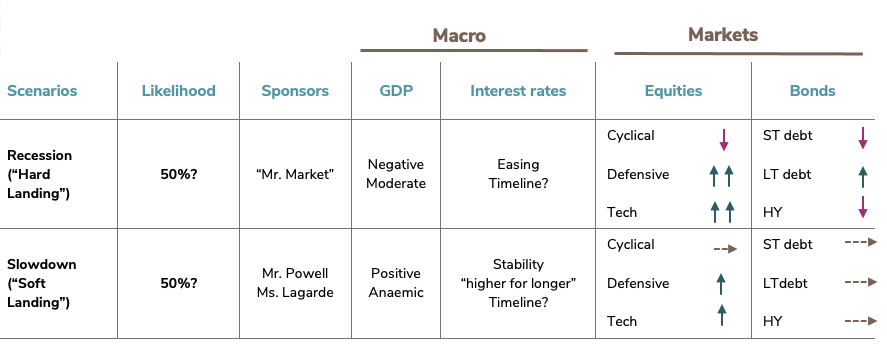

The usual macroeconomic uncertainty and the corresponding response from the central banks continue, dividing economists and investors. Table 2 provides a frame of reference for the end of 2023 and, more importantly, 2024, given that the cycle appears to be lengthening without defining either of the two scenarios cited below.

A LONGER-TERM VISION: ADAPTING TO THE NEW ENVIRONMENT

I would like to supplement the foregoing with a reflection for the coming years, the evolution of which—in our opinion—may break with the dynamics of the previous decade and affect the structure of assets in our financial portfolios.

We believe that the coming years will be a more difficult period in which to obtain real positive returns, given the convergence of the following factors:

- The impact of higher interest rates

- Structural elements that precipitate phases of higher inflation

- Positive but modest economic growth… excluding technological leaps (AI)

- A fragmented political environment conducive to populism

- Growing geopolitical tensions

This context, should it materialise, may imply positive nominal returns that—once inflation is deducted—are lower than those of the last decade, which some describe as the “Great Moderation”.

Addressing this requires no major changes in EDM’s investment style, which is characterised by investing in assets that seek wealth growth, and therefore:

- We avoid big mistakes

- We identify the best companies, meaning, those of the highest quality with the most predictable businesses that...

- ...are the most boring but effective way to obtain attractive results.

- We seek long-term appreciation rather than short-term maximisation. In other words, we use common sense.

None of this is news to our clients: What, then, will be new in this future context? Essentially the continual introduction (that is the keyword) into portfolios—regardless of investor profile—of liquid or very low volatility assets that are no longer “junk” but offer attractive returns.

Our Asset Allocation Committee (AAC) has already prudently begun this evolution, made possible by the rise in interest rates that permits: i) having near-money assets to capitalise on moments of market weakness, and ii) reducing the volatility of portfolios in an already highly volatile economic, political, and social environment.

I must insist, in closing, that this does not mean a shift toward tactical management, but rather the ongoing provision of well-remunerated assets in order to capitalise on "known unknowns".

Once again, I thank you for your confidence in us and would like to take this opportunity to inform you that the Investor Forums will be held:

In Barcelona: Monday, 13 November 2023

In Madrid: Monday, 20 November 2023

Please save the dates!

Sincerely

Carlos Llamas,

CEO