The economy: the dilemma of the central banks

- The IMF’s spring forecasts confirm an economic slowdown, but not a recession.

- The price of energy, raw materials, and metals round out the impact of the war in Ukraine, given that the country is one of the main exporters worldwide, along with Russia.

- The lion’s share of inflationary pressures are concentrated in the US, where the Federal Reserve is tightening monetary policy and aims to accelerate interest-rate hikes in 2022 and 2023.

- This shift in monetary policy is the result of abandoning a transitory view of inflation in favour of a more structural reality.

- In Europe, meanwhile, inflation stems from energy prices, that is, from the war in Ukraine, the duration of which is currently anyone’s guess.

- For its part, China is facing a sudden outbreak of COVID-19, in addition to a crisis in the real estate sector.

Markets: the bond crisis

- At the April close, declines in the price of government debt and investment-grade bonds were the deepest in decades.

- Bond markets, which are larger than stock markets, anticipate interest-rate hikes: the US Treasury yield nearly hit 3%, with the German Bund at 0.94%.

- Higher yields are due to a massive sell-off by investors who aim to protect themselves from an impending rise in interest rates.

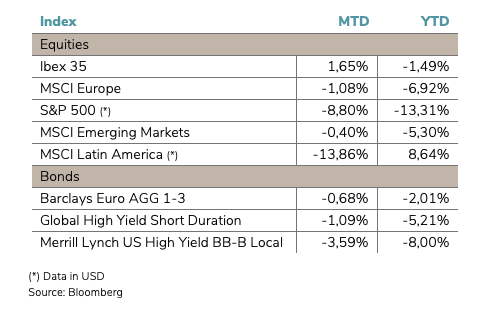

- These movements reverberate through all markets, including equity markets. The table below shows the movement of the indices at the end of the month.

- After an appreciable rebound in the second week of March, April delivered further misgivings about the near-term future.

- Of note were the substantial declines in the valuations of certain US tech companies that led stock markets in previous years.

Investment policy: good earnings reports (EPS) among equities

- Bond losses have been considerable, indicative of a painful return to a degree of normality after years of “financial repression.”

- Nevertheless, unfortunately a recovery in yields does not signify positive real returns (net of inflation).

- It is likely that, going forward, the year-on-year rate of inflation will slow, leading us to less arresting average annual levels.

- This means that, despite fears of a recession, many investors will continue to invest in equities to protect themselves from inflation that, though persistent, will not likely exceed 4% in the long term.

- The initial Q1 2022 earnings publications confirm that companies with pricing power have succeeded in safeguarding their margins through price increases. They constitute the core (75%) of those that make up EDM’s equity portfolios.

- The strength of the results presented in late April once again reassures us about long-term investment in an uncertain environment. Comforted by our conviction about the elevated quality of our portfolio, we maintain our positions in the hope that fundamentals will prevail over the current anxiety.

LEGAL CONSIDERATIONS

1) This information, which constitutes EDM advertising, is intended for informational purposes only in accordance with the rules of conduct applicable to investment services in Spain, and is therefore sufficient and understandable for any potential recipient.

The information may refer to or entail additional, separate documentation, which you may request from EDM.

If this information contains offers of products, financial instruments, or services, recipients may avail themselves to any complementary or additional documentation that enables them the comply with the terms and conditions of the offer in question.

2) EDM Gestión, S.A.U. SGIIC is a limited liability company under Spanish law registered in the CNMV’s Special Registry of Collective Investment Scheme Management Companies (Registro Especial de Sociedades Gestoras de Instituciones de Inversión Colectiva) no. 49, and in the Commercial Registry of Madrid, under volume 36,739, sheet 52, page M-658.326, with tax identification no.: A-58.217.175. Its activity includes the representation, management, and administration of Funds and Investment Companies located in Spain and subject to Spanish law, in addition to discretionary portfolio management.

3) Recipients of this information must take into account the fact that any result or data provided may be subject to fees, commissions, taxes, and expenses, which may decrease or alter the gross result, depending on the nature of each case.

4) The instruments included in this information are subject to the potential effects of several common causes, including:

-

Market fluctuations due to unforeseen circumstances.

-

Liquidity risk and other risks that alter the evolution of the investment.