Dear client,

In early 2022 investor sentiment is defined by an intense and growing uncertainty about the evolution of the pandemic and its latest Omicron variant, as well as by monetary policies in response to rising inflation.

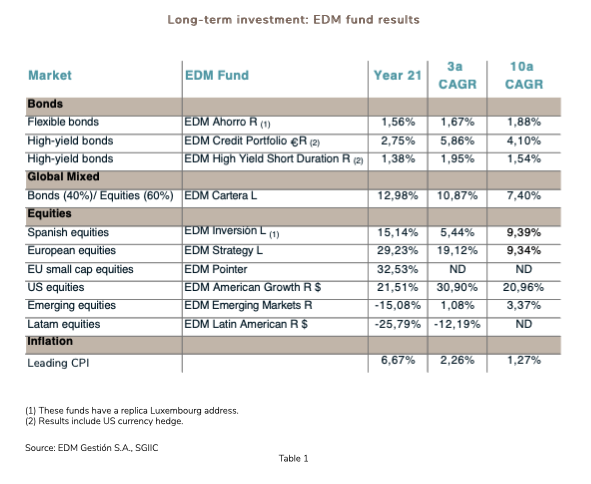

Before addressing these points, let us review the performance of your investments in 2021. Table 1 shows the results of the main EDM investment funds for the past year, over a longer time horizon, and relative to inflation.

2022 Investment Challenges

In 2022, investors must contend with three decisive issues that will likely also persist in the years to come.

1. Is growth easing? The Omicron effect

Compared to the economic downturn of 2020, the past year was one of tremendous recovery. The rebound was mixed, both by region (more intense in the US) and by sector (consumption of durable goods). However, as 2021 progressed, we saw growth shift toward 2022, when it will remain high, but lower than expected only a matter of months ago.

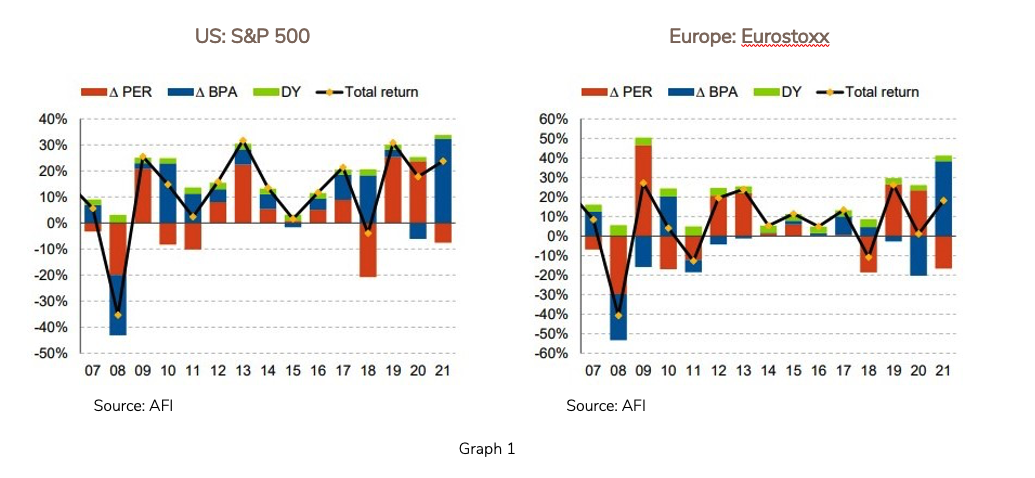

The rapid succession of the Delta and Omicron variants disproportionately affects service sector activity. This in turn impacts earnings per share (EPS), the main driver of long-term stock market appreciations, as illustrated in Graph 1, which shows that the EPS ∆ (blue bar) is the main contributor to annual investment returns, especially on the US market, posting spectacular results in the last decade.

Graph 1 illustrates that the evolution of the P/E ratio (red bar) is more volatile than that of EPS and dividends (green bar).

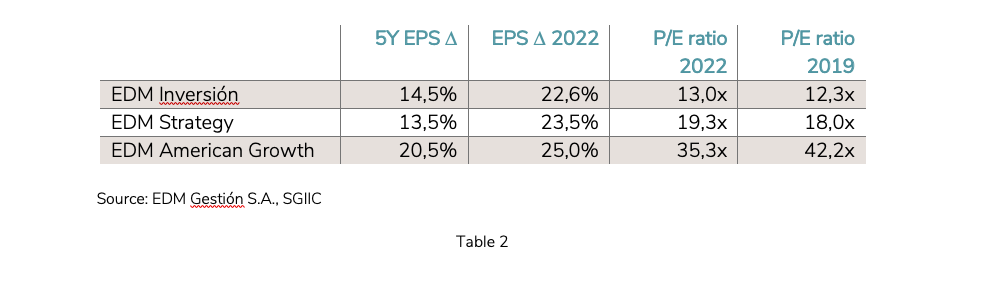

We are confident that double-digit growth will continue in 2022 (Table 2) for the companies selected by EDM.

The favourable performance we anticipate is the result of our strict stock-picking process and we are confident that results will far exceed the EPS ∆ expected by analysts for the market as a whole (6.5% - 9%). Thus, the slowdown in economic growth in 2022 should not necessarily affect our selection of companies.

Table 2 also shows that the 2022 P/E ratio is lower than (US) or similar to (Spain/Europe) that of 2019 because the intensity of the rebound in profits has eclipsed that of share prices.

2. Inflation: temporary or permanent?

With inflation at levels unseen for 40 years, markets are beginning to question its magnitude and duration. No one knows for sure. The central banks have already indicated that, although they expect inflation to ease in the second half of the year, they remain vigilant and open to tightening monetary policy if necessary in an effort to maintain their credibility as the guarantors of price stability.

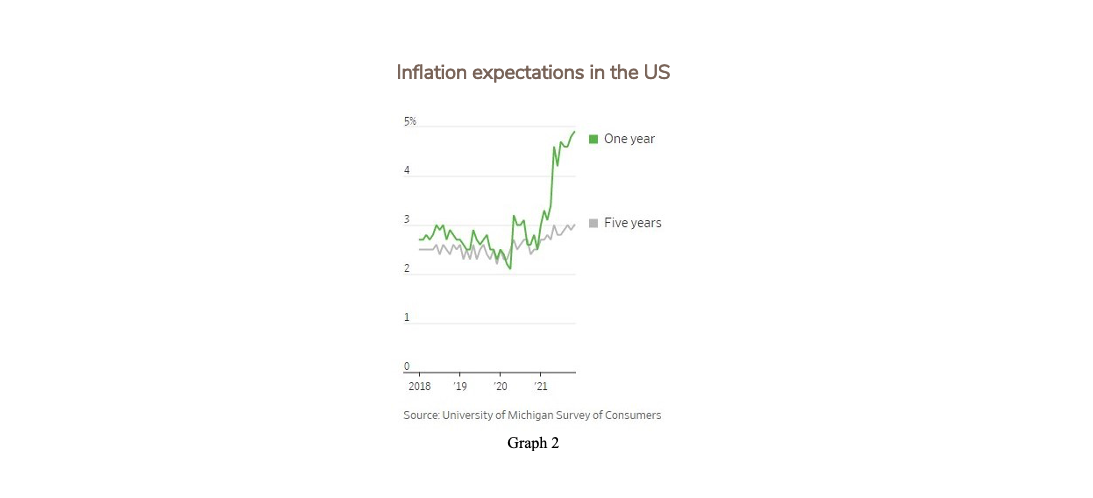

This cautious positioning may or may not materialise, depending on how inflation evolves. At the moment, investors expect to see inflation in the short term, less so in the medium term (see Graph 2). In fact, core inflation (excluding energy and food) is roughly 3% in the US and 2% in the eurozone.

Will the announced tightening of monetary policy affect the price of financial assets?

With regard to fixed income, if the central banks buy less public debt and subsequently raise interest rates, these movements may affect the required yield on 10Y bonds, the risk-free financial asset par excellence. In other words, the price would decrease as the required yield increases. This process already occurred in 2021, with several bond indices closing in negative territory.

To weather this adjustment period, we prefer to invest in short-term bonds issued by companies with established solvency, since long-term public debt is more sensitive to the evolution of inflation.

And equities? Theoretically, share valuations (P/E ratio) suffer as the performance of risk-free assets improves. This happened in 2021. Still, it is advisable to remain cautious about the future since historically this potentially adverse impact depends also on the intensity and speed of interest-rate hikes.

Moreover, inflation does not affect all companies equally. At EDM we are committed to selecting quality companies, meaning those that, among other characteristics, can increase prices to protect their margins without losing sales. Should inflation accelerate, it would be essential to harness this pricing power. We believe all of our companies have this capacity

The P/E ratio expected for our selection in 2022 does not vary substantially from that of 2019. This approach does not prevent short-term corrections, but it does ensure long-term results. And at some point in the year ahead, many emerging market shares (China, in particular) will begin to rebound from their current undervaluation.

3. Major changes worldwide

In conversations with clients that extend beyond 2022, a sense of vertigo surfaces given the many changes we are witnessing in various areas:

3.1 Energy transition

At our Investor Forum last November, professor Mariano Marzo clarified the indispensible effort needed to readjust the planet’s climate cycle. This readjustment will require major investment and considerable engagement from both companies and individuals.

3.2 Globalisation recedes

In recent years, the weight of global trade stabilised relative to world GDP. Now, after COVID, many companies are returning to their countries of origin in order to better control and secure supply chains for essential products.

3.3 How to repay a mammoth public debt?

With debt/GDP at post-WWII levels, repayment could entail three possible scenarios: (1) economic growth, (2) inflation, and (3) low or negative real rates. The latter will require governments and central banks to formally and tacitly agree on a strategy.

3.4 Social and political instability

With two major crises in just over a decade (the 2008 global financial crisis and the COVID pandemic), the fallout in terms of social instability and political radicalisation is beginning to surface. Without a doubt, the State will assume a greater role in the economy and in our lives.

In our opinion, the combination of the four previous points signals higher inflation for the next 10 years, though not very high in absolute terms. We will therefore have to adapt our portfolios as these trends materialise.

With your support, we approach 2022 with “sceptical optimism,” confident that many of our concerns will recede over time, while naturally others will appear. There is more uncertainty today than at other times in the recent past, but it will not last forever.

In the meantime, our mission is to preserve your capital and beat inflation. And we believe that the safest and most rational way to do so is to select the best bonds and equities. We entrust that task to our investment team of 16 experienced and highly motivated analysts and managers.

I would like to thank you sincerely for the trust you place in EDM and once again wish you a very happy 2022.