Dear client,

We close the books on 2022, a year in which financial markets posted their worst results in decades for both bonds and equities, with double-digit valuation losses in an environment of monetary uncertainty and geopolitical pessimism.

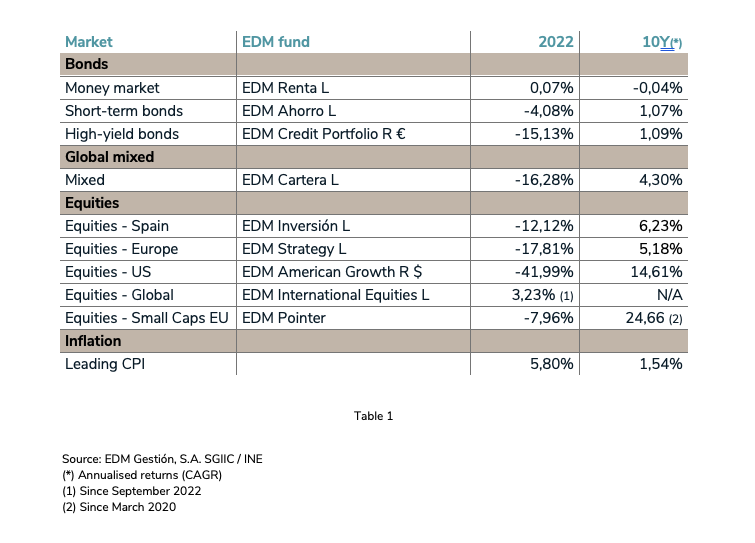

EDM fund results

Table 1 shows the results of our main funds in 2022 and their annualised returns over the last 10 years, in keeping with our stated approach as long-term investors.

Though no consolation, these data remind us that time is a long-term investor’s best ally.

The Table fails, however, to adequately illustrate the “magic of compound interest”. For example, an annualised interest rate (CAGR) of 5% would double the value of the investment in 15 years; at 6% in 12 years; at 10% in 7 years!

Our equity funds are in that range, far exceeding inflation for the period.

Equities: the inflation/recession dilemma

Financial markets have fluctuated like roller coasters in response to changing inflation and economic growth forecasts, and the reaction of the central banks, particularly the US Federal Reserve.

This has affected stock market performance (Graph 1), with the most significant declines occurring in the first half of 2022, when the outbreak of war in Ukraine and persistent inflation convinced many investors that an imminent recession loomed in the second part of the year, which did not occur.

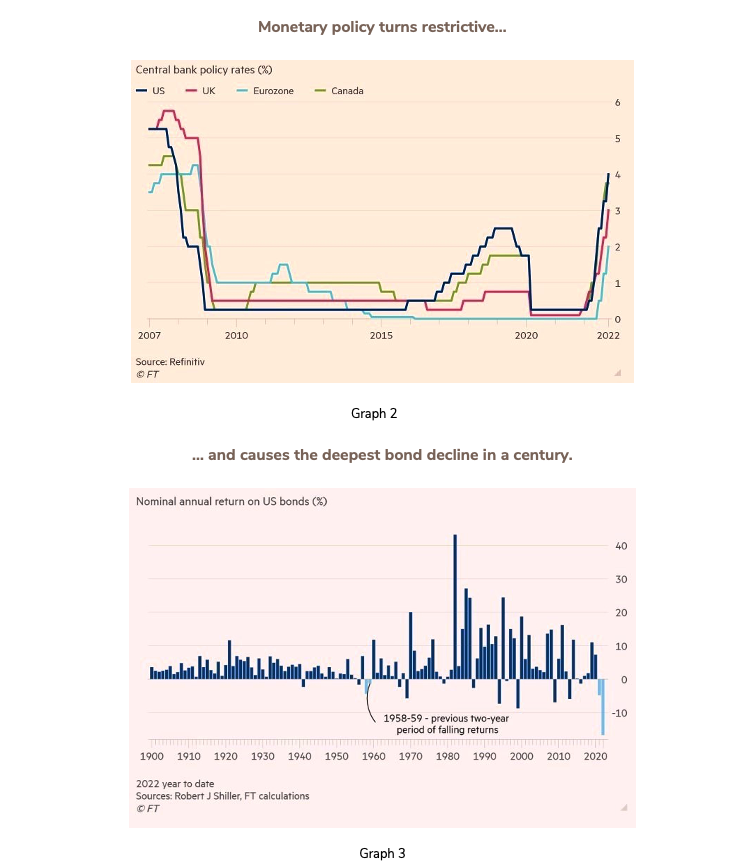

Bonds: heads and tails

Though the plunging prices of credit and sovereign bonds were the worst in the history of markets, they conceal some good news—an uptick in yields (Graphs 2 and 3)—and suggest that bonds will return to investors’ radars, once again becoming a critical ingredient in portfolio construction. After their long absence due to the super lax policies of the central banks, bonds are making a notable comeback given the monetary authorities’ determination to curb inflation.

In recent weeks we have transformed our bond portfolios to capitalise on this favourable opportunity. The ability to acquire bonds from top-quality companies at below-issue prices provides attractive returns.

Moreover, the opportunity presented by these lower prices is likely to reverse once the central banks stop raising or even cut rates in 2024.

However, it is worth noting that, although the return to positive yields is welcome to allow for the distribution of annual income, bonds will hardly be sufficient protection to offset inflation if, as appears likely, it remains above the central banks’ traditional target (2%). Graphs 4 and 5 illustrate interest-rate expectations in line with the anticipated easing of inflation.

Looking ahead to 2023: macro vs. micro

As always, expectations about stock market behaviour in 2023 are divided between optimists and pessimists, subscribing to divergent views about what drives results for listed equities: corporate profits (EPS) vs. valuation (P/E ratio).

Naturally, both views are warranted, but for investors like EDM, who are keenly aware of the individual progress of specific companies, the more pessimistic perspective, which reasons exclusively in terms of valuation, never ceases to surprise and disconcert us.

In any case, with regard to 2023, we anticipate that:

- Though possible, a sharp recovery in multiples (P/E ratio), whose declines were the main cause of valuation losses in 2022, is unlikely.

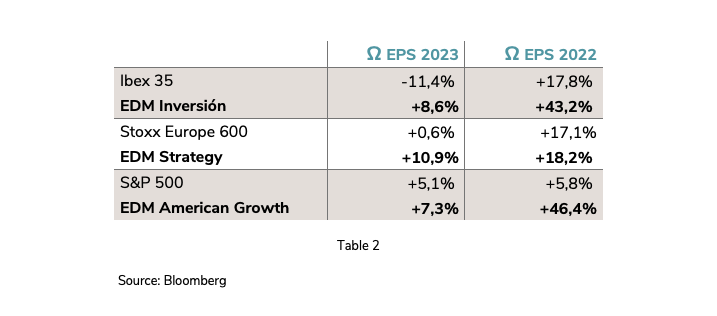

- The profit growth (EPS) of the companies in which we invest will exceed that of the indices representing their respective markets (Table 2).

Table 2 suggests that 2023 profit growth will be more moderate than in 2022, consistent with a slowing economy and taking into account the stellar results of 2022! It will, therefore, follow the path of quality and constancy that defines our style.

We can infer from the above that the data indicates moderately positive results in 2023, but our experience holds that short-term market behaviour is unpredictable and full of surprises. In contrast, over the long term, fundamentals prevail (see Table 1).

A thought to share

Those who feel disoriented and at times overwhelmed by the deterioration of institutional politics, the violence of armed conflict, and the impact of climate change, may be disappointed by the “rational optimism” of our microeconomic approach, as opposed to the “sceptical optimism” we practice with regard to macroeconomic forecasts.

That does not mean we do not share the concerns of our clients. We try, however, to approach investment in a professional and disciplined way, based on data rather than emotion. It is no easy task.

2022 has tested our clients’ patience and renewed their confidence, which we sincerely appreciate.

We strive tirelessly not to disappoint and we remain confident, as ever, that “the world will not end”.

Sincerely,

María Díaz-Morera,

Chairwoman