Dear client,

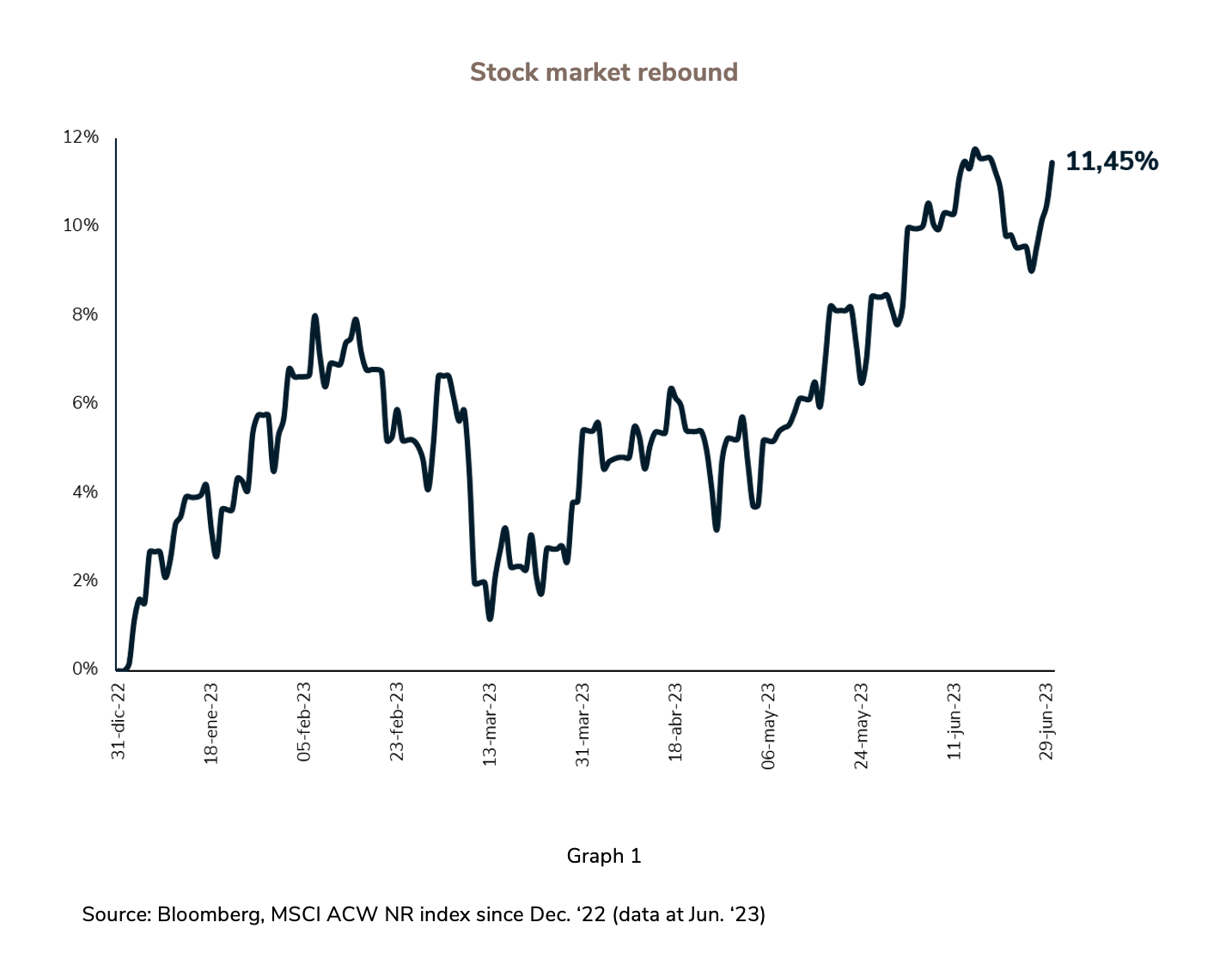

Investors face an always-odd third quarter—given its nature as a holiday period in Europe and the US—having accumulated notable appreciations since the beginning of the year and considerably more since 2022 lows, a moment of maximum pessimism. This rebound has been very intense for stock markets, as illustrated in Graph 1.

Stocks or bonds: which is the right choice?

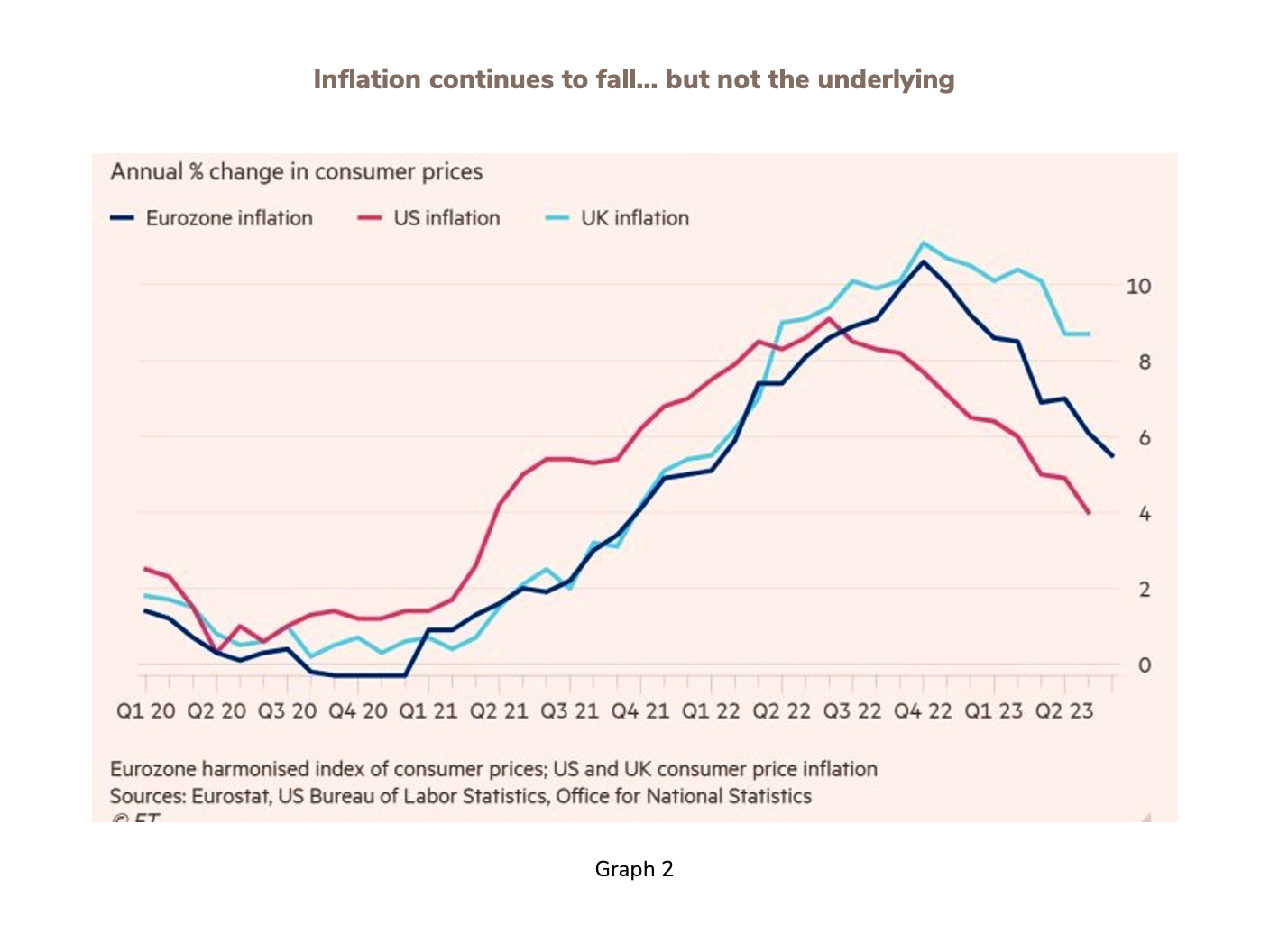

At the close of the semester, investors are split between optimists and pessimists, demonstrating the difficulty of anticipating short-term market trends. Investors are not alone, however: macroeconomists are also divided, with most predicting a recession in the US in Q4 2023/Q1 2024, though for the moment, the data does not support this hypothesis.

As history and experience dictate, when monetary policy tightens abruptly, a recession results. This is the view of bond markets and especially public debt, whose profile reflects what we call the inverted curve. The indication is that investors believe the official rates applied by the central banks to curb inflation will trigger a recession, forcing the central banks to change course. It’s a battle between Mr. Powell and Mr. Market!

Though these two perspectives are contradictory in the short term, time will likely prove one or the other—or both—correct. In the meantime, core inflation remains surprisingly resilient (Graph 2).

EDM portfolio and fund results

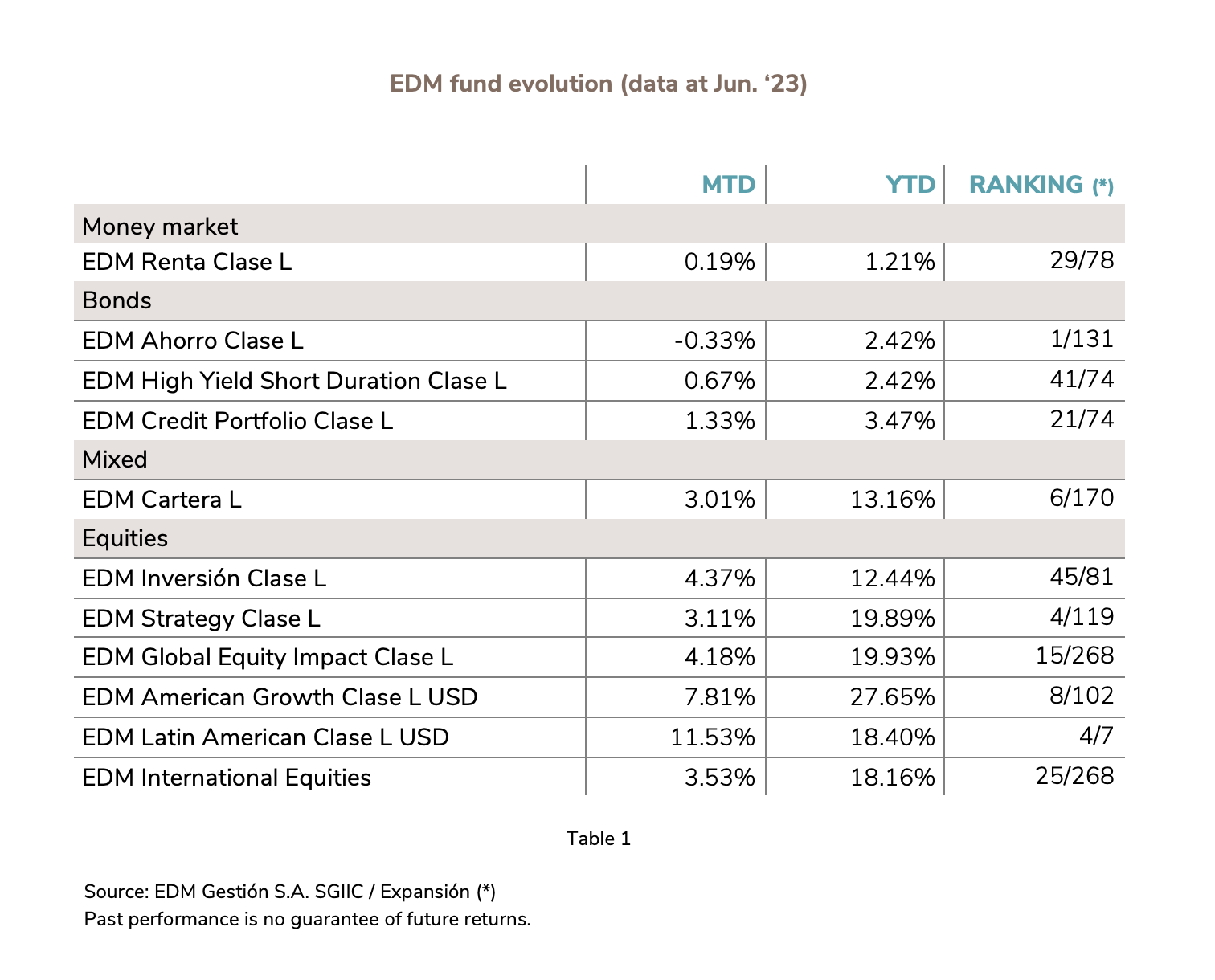

As Table 1 shows, EDM’s fund results for the first half of the year are very good, in both relative and absolute terms, allowing long-term investors to recoup much of the valuation declines in 2022 and, more importantly, contributing to the normalisation of long-term profitability (IRR/CAGR), the true objective of non-speculative investors.

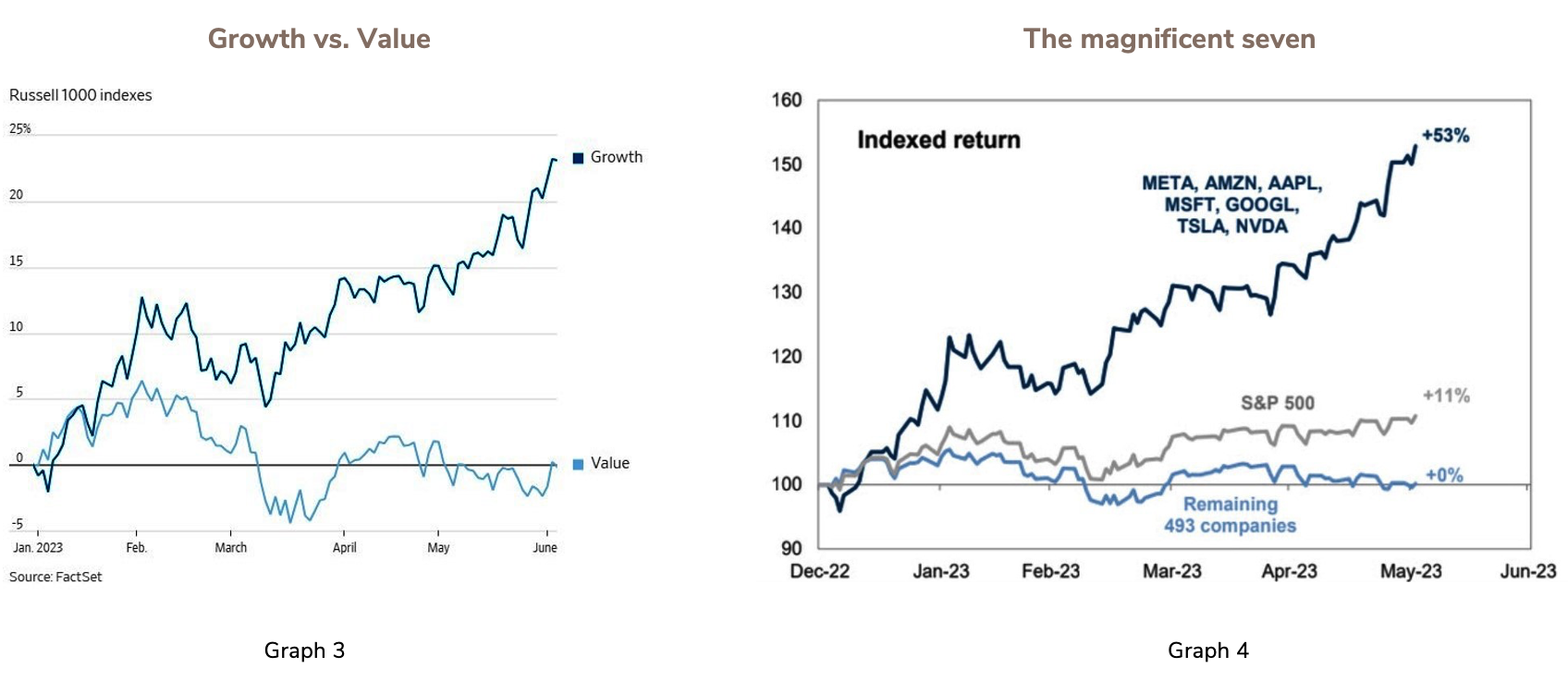

These results reflect investors’ preference for growth/defensive companies over cyclical/value companies. To a large extent, it is the opposite of what occurred in 2022. Graph 3 clearly illustrates this trend, while Graph 4 shows how it is concentrated among a small handful of tech companies, which constitute the core of EDM’s portfolios and funds.

Looking ahead: the end of a long cycle

In this biannual newsletter, I want to share EDM’s vision of what we consider will be a long-term, monetary and geopolitical shift.

After a decade of fiscal and monetary stimulus (i.e.: cash injections of incalculable sums coupled with low/negative interest rates), we are entering a converse environment that will likely be equally as long.

The new monetary environment coincides with major structural economic changes and much more active industrial policies, if only to address the challenge of climate change. We need simply add geopolitical tension to the mix to understand that proper risk remuneration, after years of secondary consideration, will prevail in the world of investment.

And whoever says risk—assuming that this return to normalcy after years of sleepiness—implies selectivity, or concentrating on the best assets, will have the winning strategy and the necessary exactitude. A more in-depth examination of this topic can be found in Eusebio Díaz-Morera’s article.

Implications for management

This vision translates to your portfolio via three principles that we discussed in the latest Opinion Flash from May:

- DIVERSIFICATION: buoyed by the return of attractive defensive (IG) bonds, absent in recent years.

- QUALITY: concentrating on businesses with maximum foreseeability.

- DISCIPLINE: rigorous in terms of valuation, to reduce or sell positions that, though justified, imply that “everything must go according to plan”.

The application of these principles underlies the results of EDM’s funds and portfolios this semester, which far exceed their respective indices, climbing to the top of the rankings (see Table 1).

So... optimists or pessimists?

As a rule, investors are not pessimists. If they were, they would withdraw from both bond and equity markets, as frequently happened among short-term investors attempting to capitalise on this year’s rebound of positive volatility.

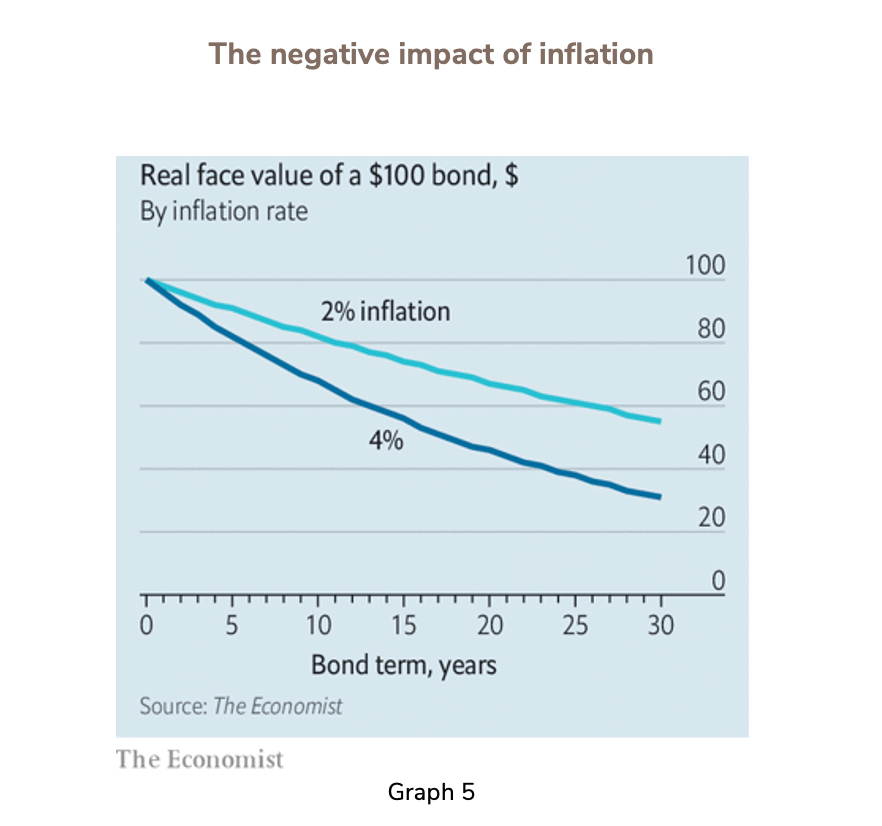

But it is important not to diverge from a strategy of investing in assets that protect against inflation, which is particularly relevant if we anticipate average inflation of 3-4% for the coming years. The cost of not hedging against inflation is considerable in the medium term, as illustrated in Graph 5.

Consequently, we are adapting our portfolios to this new environment, diversifying them into asset classes with greater or lesser volatility and alert to the opportunities that the market can offer, despite its inevitable cartwheels. For many of our clients, this means a return to the classic 60/40 equity-bond split after a period of greater equity exposure in the absence of alternatives.

I hope these words help instil some serenity at the outset of this difficult and incongruous summer season. I also hope you make the most of this time to enjoy a well-deserved break.

Many thanks again for your confidence.

María Díaz-Morera,

Chairperson

LEGAL CONSIDERATIONS

1) This information, which constitutes EDM advertising, is intended for informational purposes only in accordance with the rules of conduct applicable to investment services in Spain, and is therefore sufficient and understandable for any potential recipient. The information may refer to or entail additional, separate documentation, which you may request from EDM. If this information contains offers of products, financial instruments, or services, recipients may avail themselves to any complementary or additional documentation that enables them the comply with the terms and conditions of the offer in question.

2) EDM Gestión, S.A.U. SGIIC is a limited liability company under Spanish law registered in the CNMV’s Special Registry of Collective Investment Scheme Management Companies (Registro Especial de Sociedades Gestoras de Instituciones de Inversión Colectiva) no. 49, and in the Commercial Registry of Madrid, under volume 36,739, sheet 52, page M-658.326, with tax identification no.: A-58.217.175. Its activity includes the representation, management, and administration of Funds and Investment Companies located in Spain and subject to Spanish law, in addition to discretionary portfolio management.

3) Recipients of this information must take into account the fact that any result or data provided may be subject to fees, commissions, taxes, and expenses, which may decrease or alter the gross result, depending on the nature of each case.

4) The instruments included in this information are subject to the potential effects of several common causes, including:

- Market fluctuations due to unforeseen circumstances.

- Liquidity risk and other risks that alter the evolution of the investment.

5) This information contains data that reflect the past performance of the cited products. The data is a reference or record used to reach a conclusion, but is in no way an indisputable indicator of future performance.

6) This documentation may contain data based on currencies foreign to the recipient. Therefore, the possibility of an upward or downward fluctuation in the value of the currency and its effect on the results of the proposed product or instrument should be taken into account.

7) To ensure discretionary portfolio management services are provided within the scope of suitability, MIFID regulations require EDM to collect the necessary information regarding its clients’ investment goals, financial capacity and investment experience and knowledge. To that end, EDM will obtain the information needed to create an investment profile of each client, consistent with their particular circumstances. Regulation does not permit EDM to render discretionary portfolio management services without the information necessary to assess the suitability of its clients.

8) To obtain the mandatory legal information, please visit the website of the management company EDM Gestión, S.A.U. SGIIC at www.edm.es. You may also obtain a hard copy of this information upon request, free of charge.